How to Calculate Financial Ratios From a 10-K: Step-by-Step

By Chad Hartman

Published June 21, 2026 · Last updated June 21, 2026

Type "how to calculate financial ratios" into a search engine and most of what comes back is a formula sheet: Current Ratio equals this divided by that, Debt-to-Equity equals this over that. What almost none of those guides show is where those inputs actually live inside a real filing — which line, under which header, reported under which XBRL tag — and that gap is exactly where most self-taught investors get the math wrong. This guide closes it. Using Apple's most recently filed 10-Q — Q2 FY2026 (filed May 1, 2026, period ending March 28, 2026) — we will build four ratios directly from the as-filed balance sheet, income statement, and cash flow statement: one liquidity ratio, one leverage ratio, one profitability ratio, and one valuation ratio. Every input traces to a specific filing line. Every formula is built by hand before it gets checked against the platform number.

Table of Contents

- Step 1: Find the Filing and the Exact Line Item

- Step 2: Calculate a Liquidity Ratio — The Current Ratio

- Step 3: Calculate a Leverage Ratio — The Debt-to-Equity Ratio

- Step 4: Calculate a Profitability Ratio — Gross Profit Margin

- Step 5: Calculate a Valuation Ratio — Free Cash Flow Yield

- Step 6: Reconcile Your Number Against the Platform

- Where This Process Breaks Down at Scale

- Frequently Asked Questions

Step 1: Find the Filing and the Exact Line Item

Before any formula gets touched, two decisions determine whether the resulting ratio is accurate or quietly wrong: which filing, and which line within it. A 10-K is the annual report — audited, comprehensive, filed once a year. A 10-Q is the quarterly update — unaudited, narrower in scope, filed three times a year between annual reports. The line items and the math are the same in both; what changes is the reporting period and the level of detail surrounding it. For a full breakdown of what each filing includes, see 10-K vs. 10-Q: What's the Difference?

The reason "which line" matters as much as "which filing" is that companies do not all label the same concept the same way — one company's "Term Debt" is another's "Long-Term Debt, Current Portion." The only way to know you have the right number is to match it to its XBRL tag, the machine-readable identifier every public company attaches to every reported figure under SEC rules. For a primer on how this tagging system works, see What Is XBRL? The on-screen label can shift between filings; the tag does not.

For this walkthrough, every figure comes from Apple's Q2 FY2026 10-Q, pulled directly from GeminIQ's Financial Statements view rather than a normalized summary. The balance sheet figures below reflect the filing period ending March 28, 2026.

Step 2: Calculate a Liquidity Ratio — The Current Ratio

What Is the Current Ratio?

The Current Ratio answers a narrow question: for every dollar a company owes in the next twelve months, how many dollars of short-term assets does it have on hand to cover it? It is the most commonly cited liquidity ratio because it requires only two inputs, both of which sit near the top of every balance sheet.

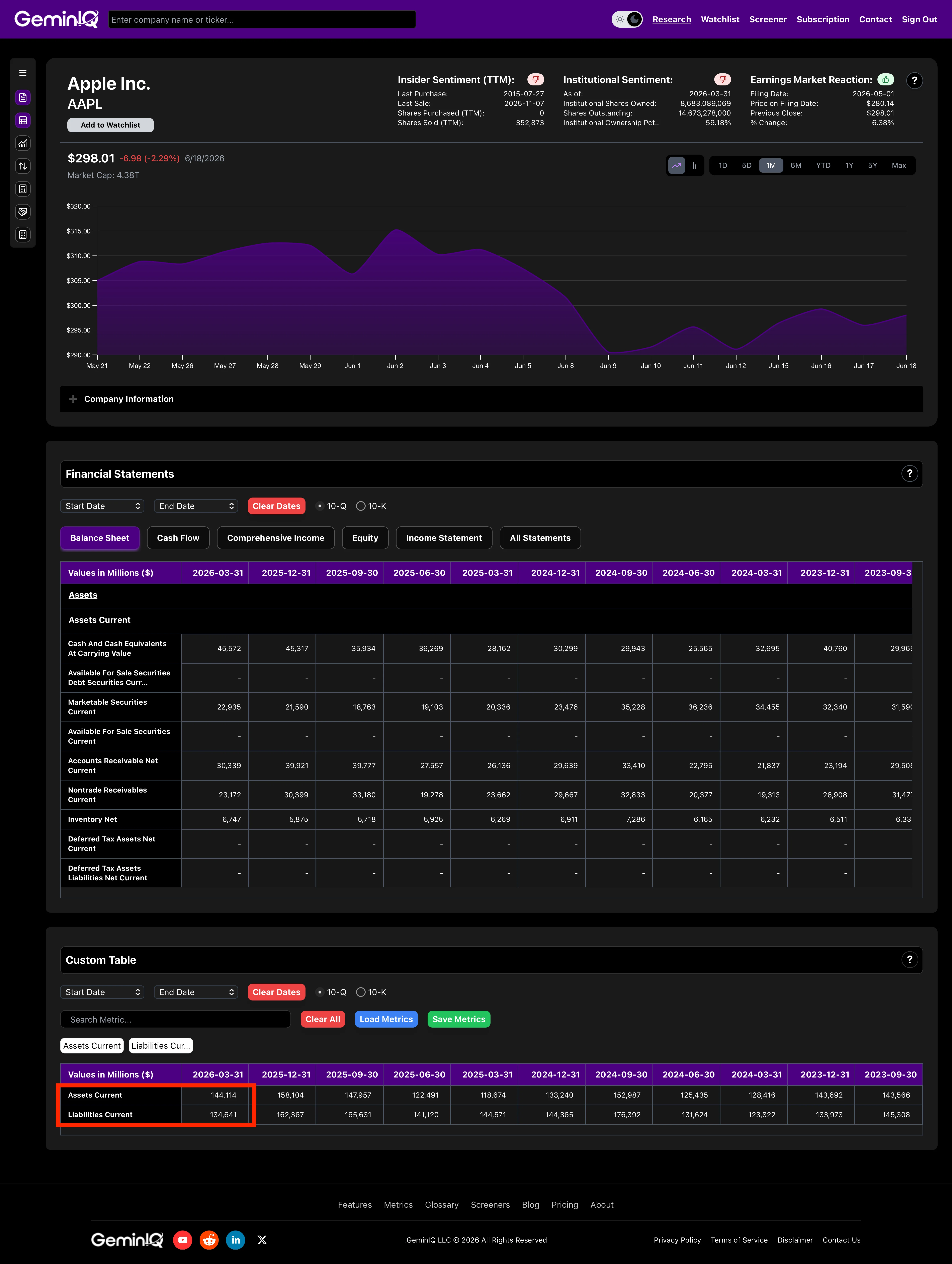

Current Ratio = Current Assets / Current Liabilities

The Data: On Apple's Q2 FY2026 balance sheet, Total Current Assets ("Total Current Assets," XBRL tag AssetsCurrent) total $144.1 Billion, and Total Current Liabilities ("Total Current Liabilities," XBRL tag LiabilitiesCurrent) total $134.6 Billion. Divide one by the other:

$144.1 Billion ÷ $134.6 Billion = 1.07

A current ratio of 1.07 means Apple holds $1.07 in current assets for every $1.00 of current liabilities due within the year — a thin but positive cushion.

When it breaks: The current ratio treats every current liability as an equally urgent cash obligation, which is not always true. A subscription or hardware-and-services business with large deferred revenue on the balance sheet can show a current ratio that looks weaker than its actual liquidity. Deferred revenue represents cash the company has already collected — not cash it still owes. The ratio is also not comparable across industries without context. A grocery chain operating with a current ratio below 1.0 is often showing operating efficiency, not distress — it collects cash from customers before it has to pay suppliers.

Step 3: Calculate a Leverage Ratio — The Debt-to-Equity Ratio

What Is the Debt-to-Equity Ratio?

The Debt-to-Equity Ratio measures how much of a company's asset base is financed by liabilities versus by shareholders' own capital. A ratio above 1.0 means liabilities exceed equity; below 1.0, equity exceeds liabilities.

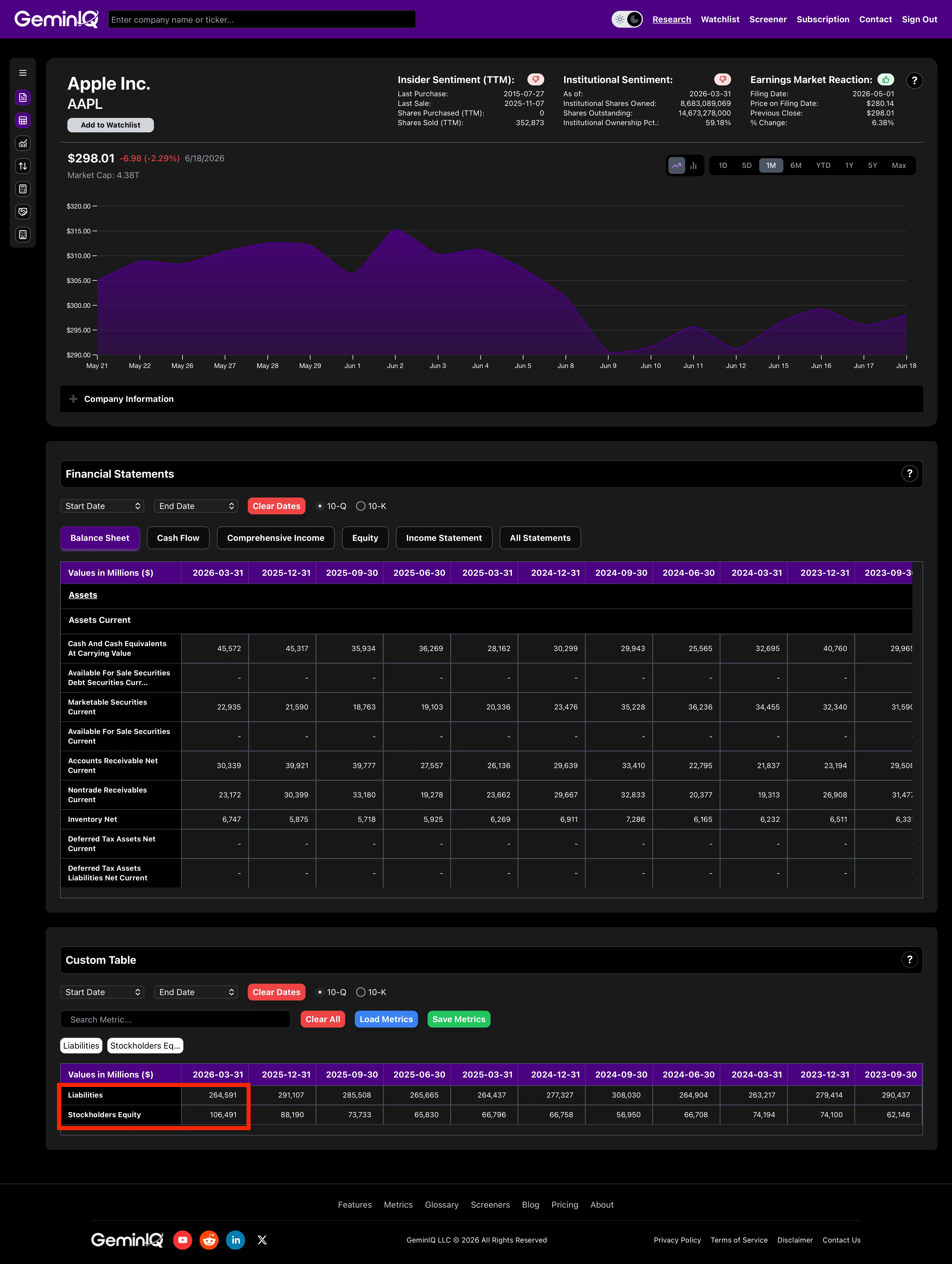

Debt-to-Equity Ratio = Total Liabilities / Total Shareholders' Equity

The Data: Apple's balance sheet reports Total Liabilities ("Total Liabilities," XBRL tag Liabilities) of $264.6 Billion and Total Shareholders Equity ("Total Shareholders Equity," XBRL tag StockholdersEquity) of $106.5 Billion.

$264.6 Billion ÷ $106.5 Billion = 2.48

Apple's debt-to-equity ratio of 2.48 means total liabilities run nearly two-and-a-half times shareholders' equity.

When it breaks: Debt-to-equity lumps every liability together, but most line items inside Total Liabilities have nothing to do with financial leverage in the way the ratio's name implies. Of Apple's $264.6 Billion in Total Liabilities, only about $84.7 Billion — Commercial Paper (CommercialPaper: $2.0 Billion) plus Term Debt, current and non-current (LongTermDebtCurrent and LongTermDebtNoncurrent: $8.3 Billion and $74.4 Billion) — is actual interest-bearing debt. The remaining roughly $179.9 Billion is operating liabilities: Accounts Payable (AccountsPayableCurrent: $57.3 Billion), Deferred Revenue (ContractWithCustomerLiabilityCurrent: $9.3 Billion), and other current and non-current obligations that carry no interest rate at all. A standard screener flags a high debt-to-equity ratio as financial risk, but pulling the raw balance sheet shows a company can carry a high ratio almost entirely through operating liabilities rather than borrowed money. The ratio is also undefined for companies with negative equity — a position several large, profitable companies have reached through aggressive buyback programs — at which point it loses its interpretive value entirely.

Step 4: Calculate a Profitability Ratio — Gross Profit Margin

What Is Gross Profit Margin?

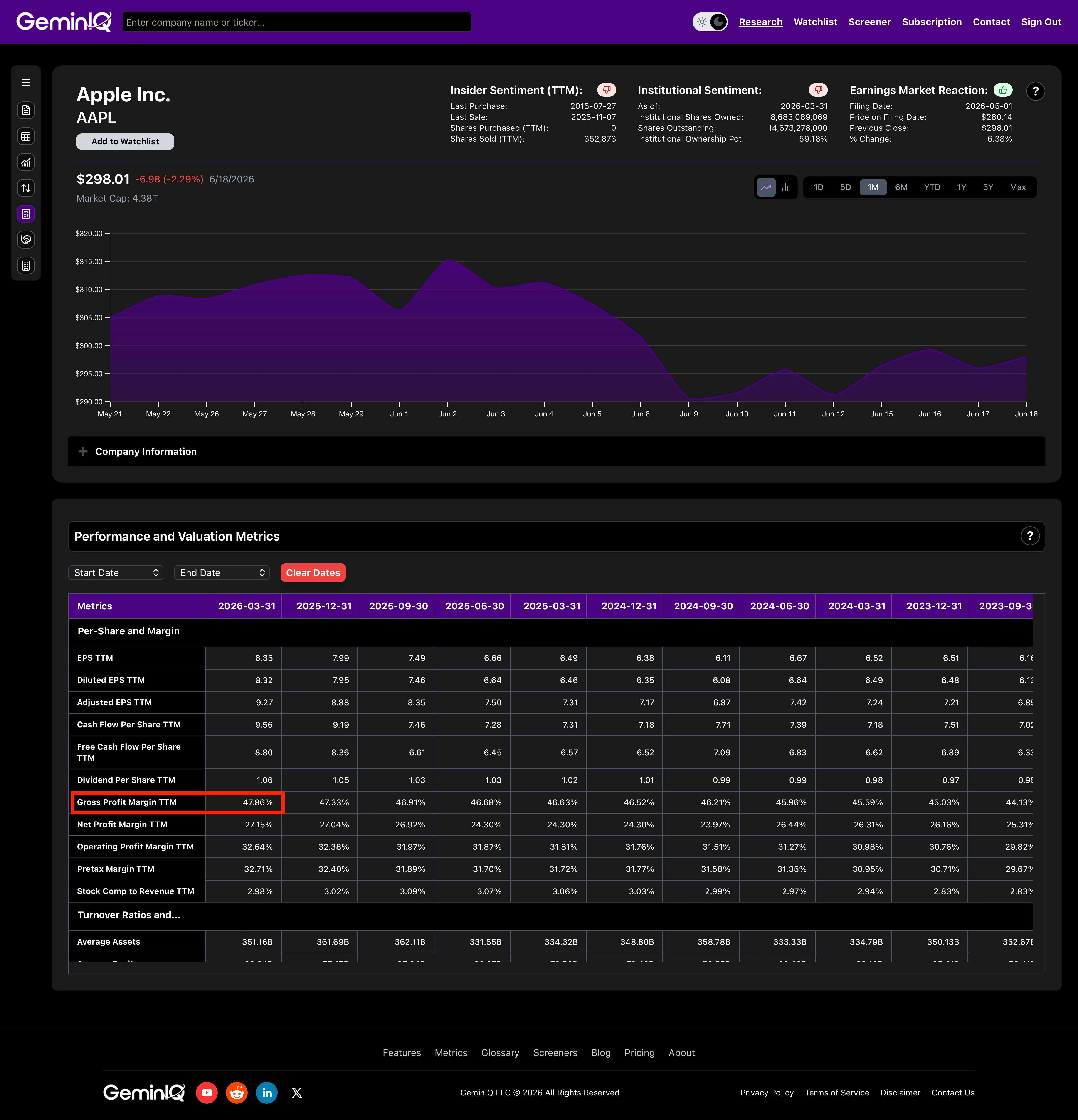

Gross Profit Margin measures what share of revenue survives after the direct cost of producing the goods or services sold. GeminIQ's Gross Profit Margin is a trailing-twelve-month calculated metric — distinct from the single-quarter "Gross Margin" line item a company reports on its income statement each period.

Gross Profit Margin (TTM) = Gross Profit (TTM) / Revenue (TTM)

The Data: Apple's Q2 FY2026 income statement reports a quarterly "Gross Margin" line (XBRL tag GrossProfit) of $54.8 Billion against Total Revenues (Revenues) of $111.2 Billion. Divide those two figures and the quarter-only margin comes out to 49.27% — and that number is already a trap. A single quarter is not a representative sample. Summing the same two line items across the trailing four quarters gives Gross Profit (TTM) of $216.1 Billion against Revenue (TTM) of $451.4 Billion:

$216.1 Billion ÷ $451.4 Billion = 47.86%

The TTM-correct figure of 47.86% sits nearly a full percentage point and a half below the quarter-only shortcut. That gap is the difference between a number reflecting a full operating cycle and one reflecting whatever seasonal mix happened to land in a single thirteen-week window.

When it breaks: Gross margin comparisons also break down across companies that classify costs differently. Some fold depreciation and amortization into Cost of Goods Sold; others report it separately below the gross profit line. Two businesses with identical underlying economics can show different gross margins purely because of where a non-cash charge gets classified — a distinction the ratio itself never reveals.

For a deeper look at what gross margin reveals about business model strength across industries, see Gross Profit Margin: What It Reveals About Business Model Strength.

Step 5: Calculate a Valuation Ratio — Free Cash Flow Yield

What Is Free Cash Flow Yield?

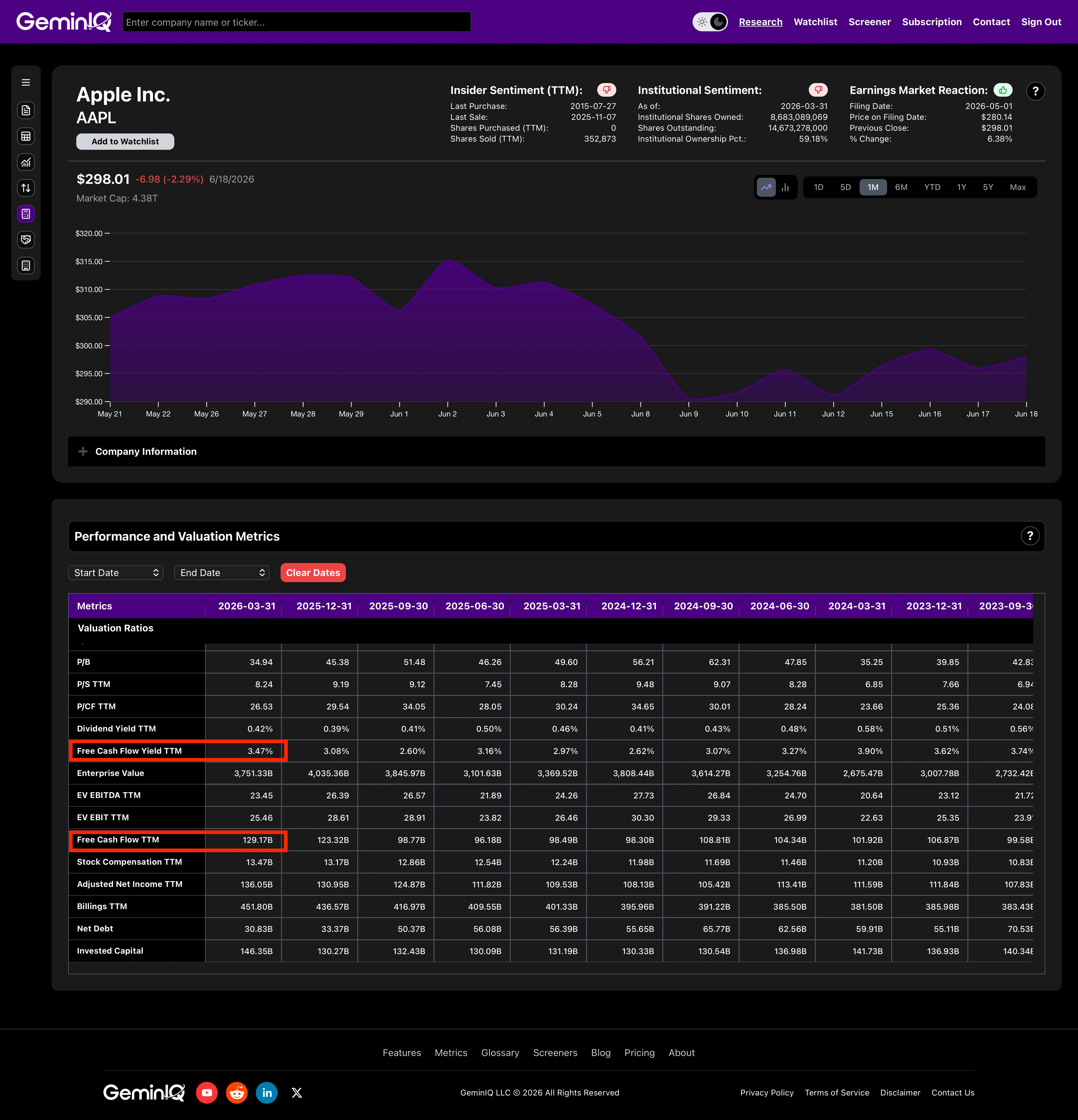

Free Cash Flow Yield expresses a company's free cash flow as a percentage of its market capitalization — effectively, how much cash the business generates for every dollar of its current price tag. It requires building one calculated metric, Free Cash Flow, before dividing it by Market Capitalization.

Free Cash Flow = Operating Cash Flow (TTM) − Capital Expenditures (TTM) Free Cash Flow Yield (TTM) = Free Cash Flow (TTM) / Market Capitalization

The Data: Apple's cash flow statement reports Cash Generated By Operating Activities (XBRL tag NetCashProvidedByUsedInOperatingActivities) and Payments For Acquisition Of Property, Plant And Equipment (XBRL tag PaymentsToAcquirePropertyPlantAndEquipment). Summed across the trailing four quarters, Operating Cash Flow (TTM) totals $140.2 Billion and Capital Expenditures (TTM) totals $11.0 Billion:

$140.2 Billion − $11.0 Billion = $129.2 Billion in Free Cash Flow (TTM)

With Apple's Market Capitalization at $3.72 Trillion, dividing free cash flow by market cap gives:

$129.2 Billion ÷ $3.72 Trillion = 3.47%

A Free Cash Flow Yield of 3.47% means Apple generates roughly 3.5 cents of free cash for every dollar of its current market value.

When it breaks: Market capitalization moves every trading day; the cash flow data behind it updates only once a quarter. A stock that has rallied sharply since its last filing will show an artificially compressed FCF yield against a current price, even though nothing about its underlying cash generation has changed — the denominator moved, not the business. The ratio can also penalize capital-intensive growth companies unfairly, since it makes no distinction between maintenance capex (spending required just to sustain the business) and growth capex (discretionary spending to expand it).

Step 6: Reconcile Your Number Against the Platform

The discipline that separates a reliable by-hand calculation from a guess is checking it against a second source before trusting it. Every figure built above — Current Ratio 1.07, Debt-to-Equity 2.48, Gross Profit Margin (TTM) 47.86%, Free Cash Flow Yield (TTM) 3.47% — matches exactly what appears in GeminIQ's Calculated Metrics view for Apple, because both the manual math and the platform figure trace back to the same as-filed line items.

That reconciliation is not guaranteed on every platform. Two financial websites showing different debt-to-equity or FCF yield figures for the same company in the same period are not necessarily making an error — they may simply be using different definitions of "total debt" or "capex" without labeling the difference. For a deeper walkthrough of how to spot-check a platform's figures line by line, see How to Verify Financial Data Against an SEC Filing — and for a closer look at where those definitional gaps come from in the first place, see Third-Party Financial Data: What Gets Lost When the Data Is Processed.

Where This Process Breaks Down at Scale

Building four ratios for one company by hand, as above, takes maybe twenty minutes once the filing is open. Building the same four ratios for fifty companies — correctly, with TTM aggregation, correctly matched current vs. non-current debt, correctly summed quarterly cash flows — does not scale linearly. It scales into hours of manual line-item hunting, and every hour adds another opportunity for a misread label or a stale quarter to slip into the math.

This is the specific problem GeminIQ's Calculated Metrics library solves. The same as-filed inputs and the same formulas used in this walkthrough run automatically, consistently, across every company in the database — current ratio, debt-to-equity, gross profit margin, free cash flow yield, and more than fifty other metrics, recalculated the moment a new filing posts. Once you can calculate a ratio by hand, the Stock Screener becomes the tool for asking the same question across the entire market: which companies clear a current ratio above 1.5, a debt-to-equity below 1.0, or a free cash flow yield above 5%, all at once.

For the metric that goes one level deeper than any single ratio here — combining profitability and capital efficiency into a single number — see Return on Invested Capital (ROIC): Formula and Benchmarks.

Frequently Asked Questions

Does this process work the same way for a 10-K as it does for a 10-Q?

Yes. The line items, the XBRL tags, and the formulas are identical between the two filing types. The only difference is reporting cadence — a 10-K covers a full, audited fiscal year, while a 10-Q covers one unaudited quarter with year-over-year comparisons. TTM ratios like Gross Profit Margin or Free Cash Flow Yield are built the same way regardless of which filing type supplied the most recent quarter.

Why do some ratios use a single period and others use TTM?

Balance sheet ratios like the current ratio and debt-to-equity ratio are snapshots — they describe a company's position on one specific date, so a single period is correct by definition. Income statement and cash flow ratios like gross profit margin and free cash flow yield are flow measures, and a single quarter can be skewed by seasonality. Summing the trailing four quarters smooths that distortion into a figure that better represents a full operating cycle.

Can I calculate these ratios without a paid data platform?

Yes. Every input in this guide is publicly available on SEC EDGAR for free. The tradeoff is time: locating the correct line item across dozens of possible label variations, summing four quarters by hand for every TTM metric, and repeating the process for every company under analysis. A platform that pre-calculates these metrics from the same as-filed data removes the manual labor without changing the underlying math.

Why might my by-hand calculation differ from a number I see on a different financial website?

The formula is rarely the source of disagreement — the definition of an input usually is. "Total debt" can mean only interest-bearing instruments or it can mean total liabilities, depending on the platform. "Capex" can include or exclude capitalized software development costs. If a by-hand calculation built from as-filed figures does not match a platform's displayed number, the input definitions disagree — not the filing.

Research Faster. Invest Smarter.

Most financial websites rely on third-party aggregators that simplify or process data before you ever see it. We built GeminIQ because we believe you deserve a better fundamental analysis tool—one that goes beyond basic price charts and processed numbers. We extract our data directly from SEC 10-K and 10-Q filings to ensure that when you look at a balance sheet or a cash flow statement, you are seeing the numbers exactly how the company reported them. Our goal is to give you the tools to verify the narrative for yourself using clean, traceable data. Start researching now at GeminIQ.com.

All financial figures cited in this article reference Apple Inc.'s Q2 FY2026 10-Q (filed May 1, 2026, period ending March 28, 2026). All SEC filings are publicly available at SEC EDGAR.

Disclaimer: The content in this blog is for educational and entertainment purposes only and does not constitute financial, legal, or tax advice. Investing involves risk, including the loss of principal. The views expressed are my own and not intended as financial advice or a guarantee of future performance.