Intel Stock Analysis 2026: What the Q1 10-Q Actually Shows

By Chad Hartman

Published June 18, 2026 · Last updated June 18, 2026

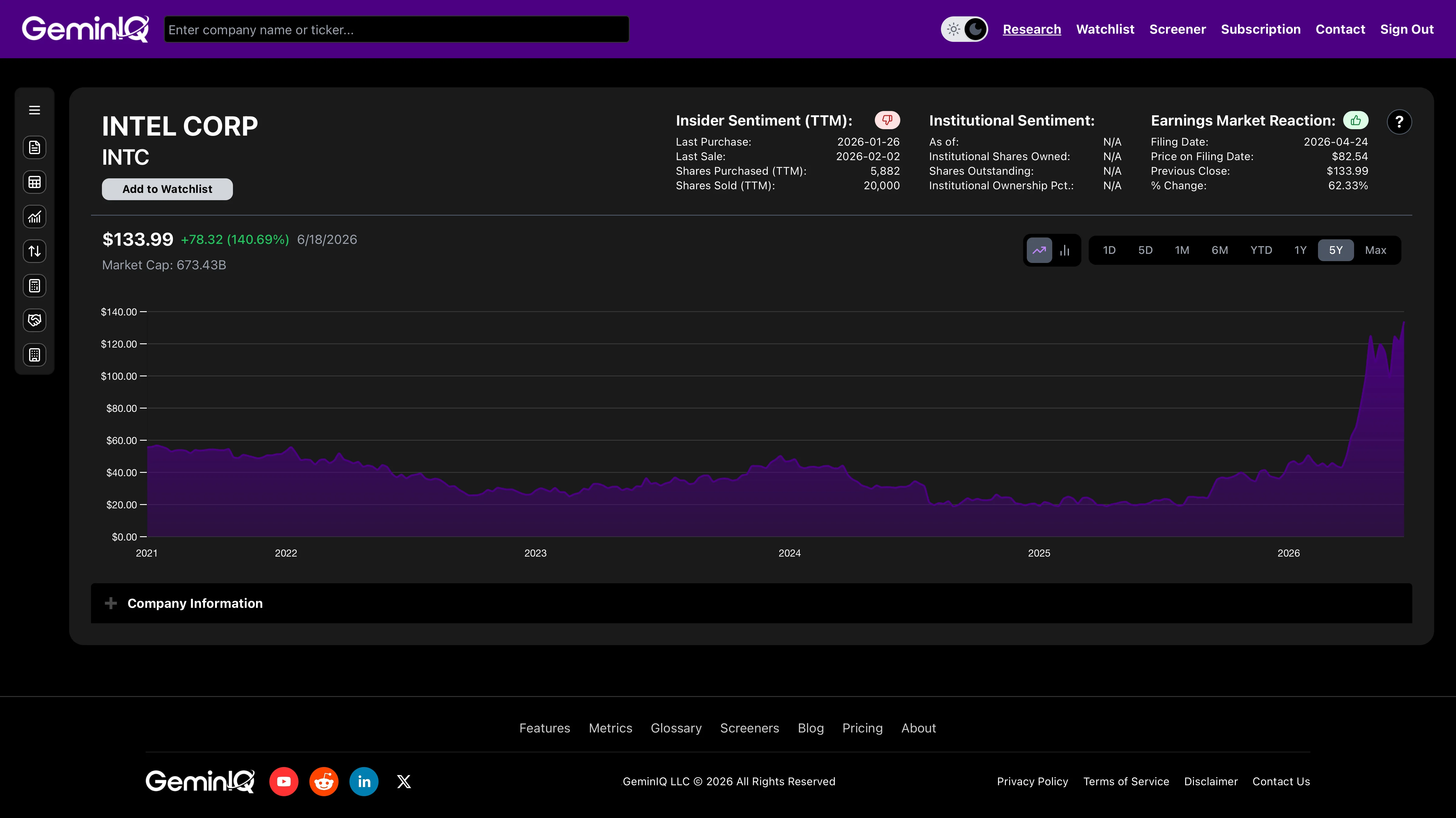

Intel ($INTC) just filed its Q1 FY2026 10-Q (filed April 24, 2026, period ending March 31, 2026), and the financial media is not reading it. The narrative — AI comeback, Computex momentum, Foxconn partnership, 18A process node, full-stack reinvention — drove the stock from roughly $30 to a peak near $135, one of the most dramatic reversals of 2026. But the income statement, the cash flow statement, and GeminIQ's raw SEC data tell a different story. Revenue has fallen 33% from its peak. Free cash flow is negative. The company took $4.07 billion in restructuring charges in a single quarter. And the trailing twelve-month Return on Invested Capital sits at -3.4%. Here is the fundamental, data-driven truth behind the ticker.

The Revenue Collapse the Rally Is Trying to Forget

The financial media covers Intel as a comeback story. The raw income statement tells you how far there is still to go.

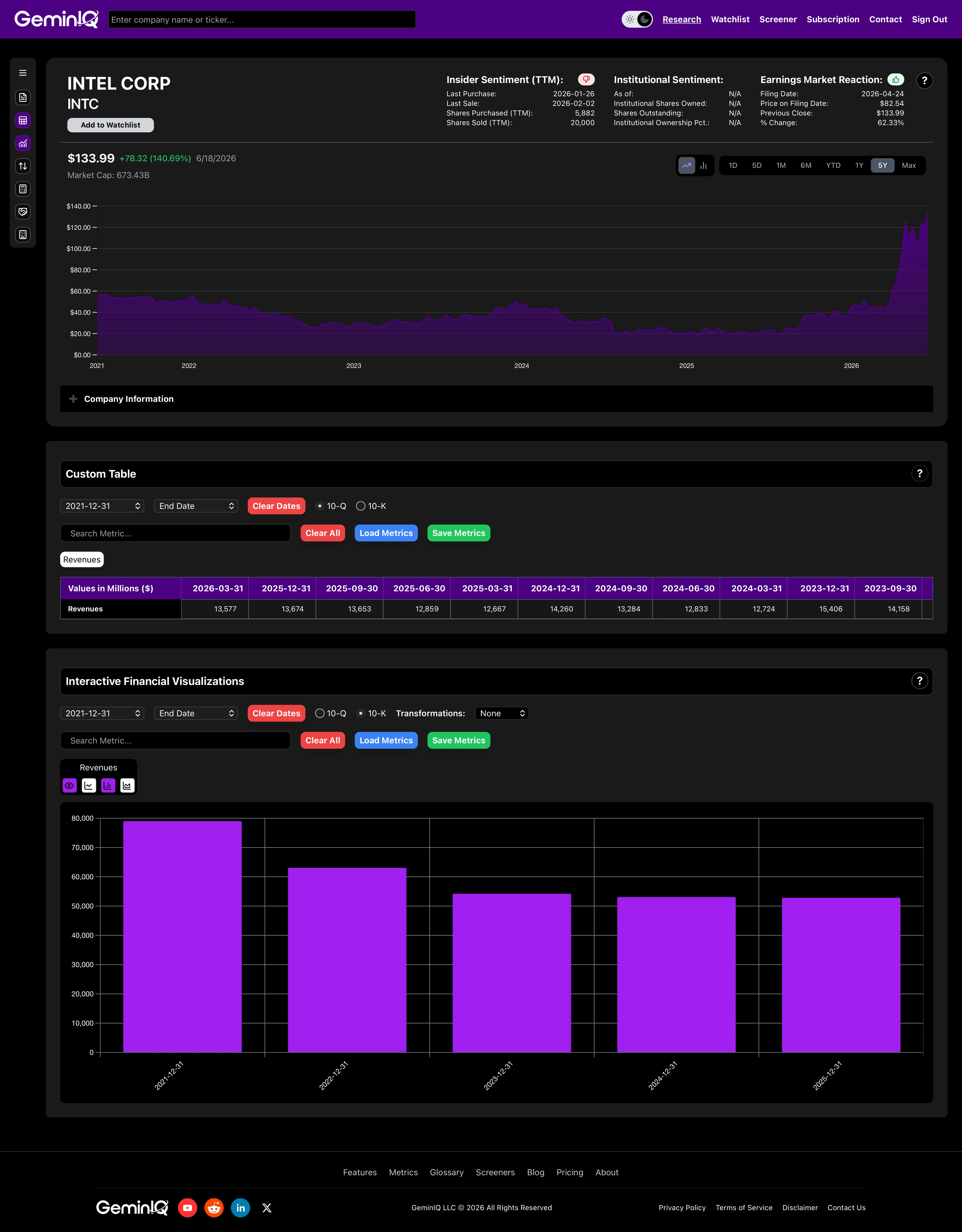

The Data: In FY2021, Intel generated $79.024 Billion in total revenues (Revenues). By FY2022 that had fallen to $63.054 Billion. FY2023 brought $54.228 Billion. FY2024 came in at $53.101 Billion. FY2025 was $52.853 Billion — barely moved from the year before. Q1 FY2026 posted $13.577 Billion in quarterly revenue, which annualizes to approximately $54.3 Billion. Three years of restructuring and billions in capital investment have not reversed a -33% revenue decline from peak.

The GeminIQ Edge: Pulling Intel's Revenues line directly from the raw financial statements in GeminIQ makes the trajectory unmistakable. Standard aggregators often present trailing-twelve-month figures that smooth this decline. The period-by-period filing data does not.

Gross Margin: The One Signal Worth Paying Attention To

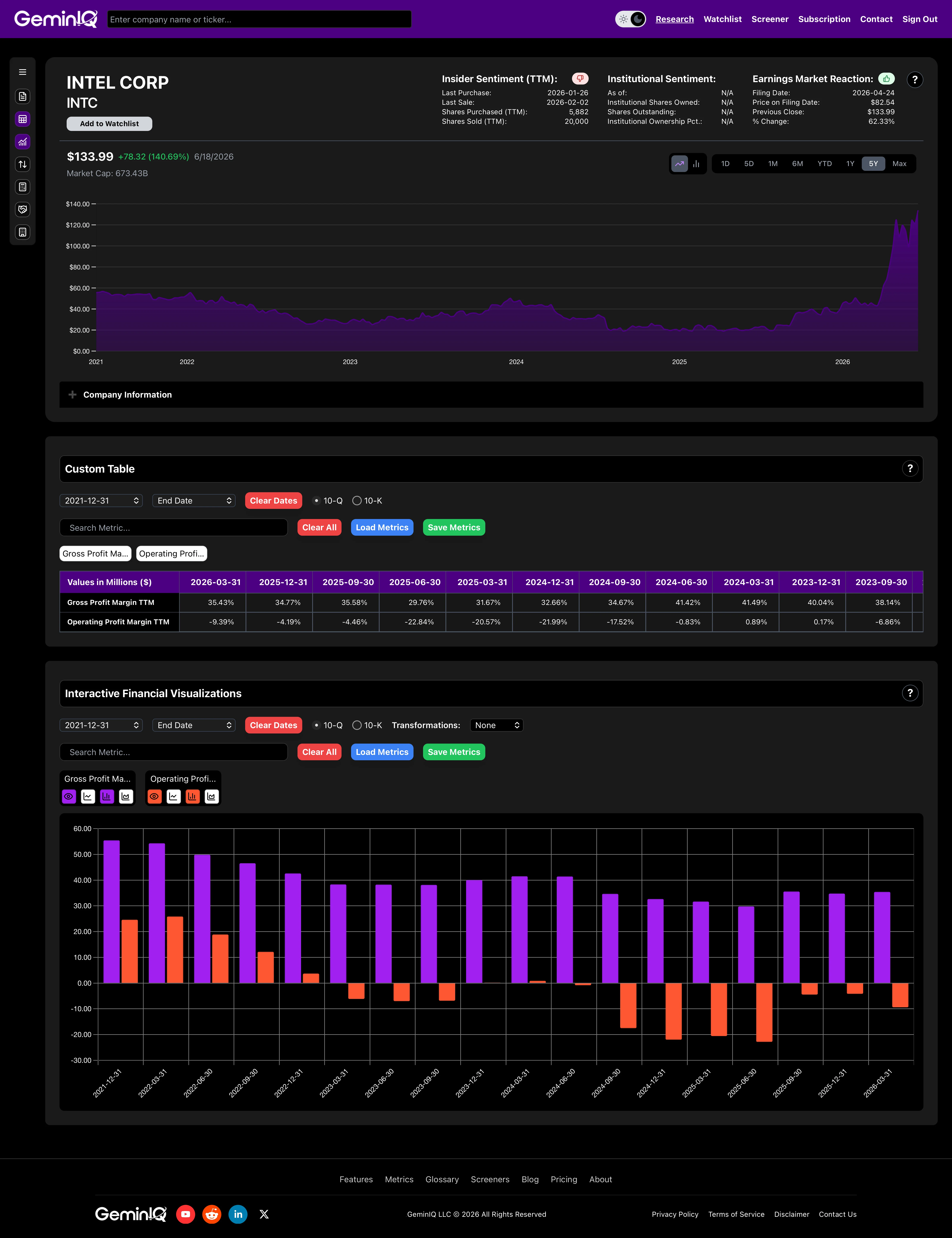

Not everything in the filing is bad news. One metric has improved in a way worth noting, and it is worth separating from the noise.

The Data: Intel's Gross Profit Margin (GrossProfit ÷ Revenues) collapsed from 55.4% in FY2021 to 32.7% in FY2024 as the company absorbed massive fab depreciation and underutilization costs. FY2025 showed a recovery to 34.8%. Q1 FY2026 reached 39.4% — the highest quarterly gross margin in three years. Gross profit for the quarter was $5.347 Billion on $13.577 Billion in revenue, leaving $934 million in operating income before restructuring charges. The manufacturing cost story is, slowly, improving.

The GeminIQ Edge: GeminIQ's pre-calculated Gross Profit Margin surfaces this recovery in seconds. Viewing it alongside the Operating Profit Margin makes the remaining gap plain: gross margin is recovering, but operating losses persist — the spending has not caught up to the improvement.

The Restructuring That Never Ends

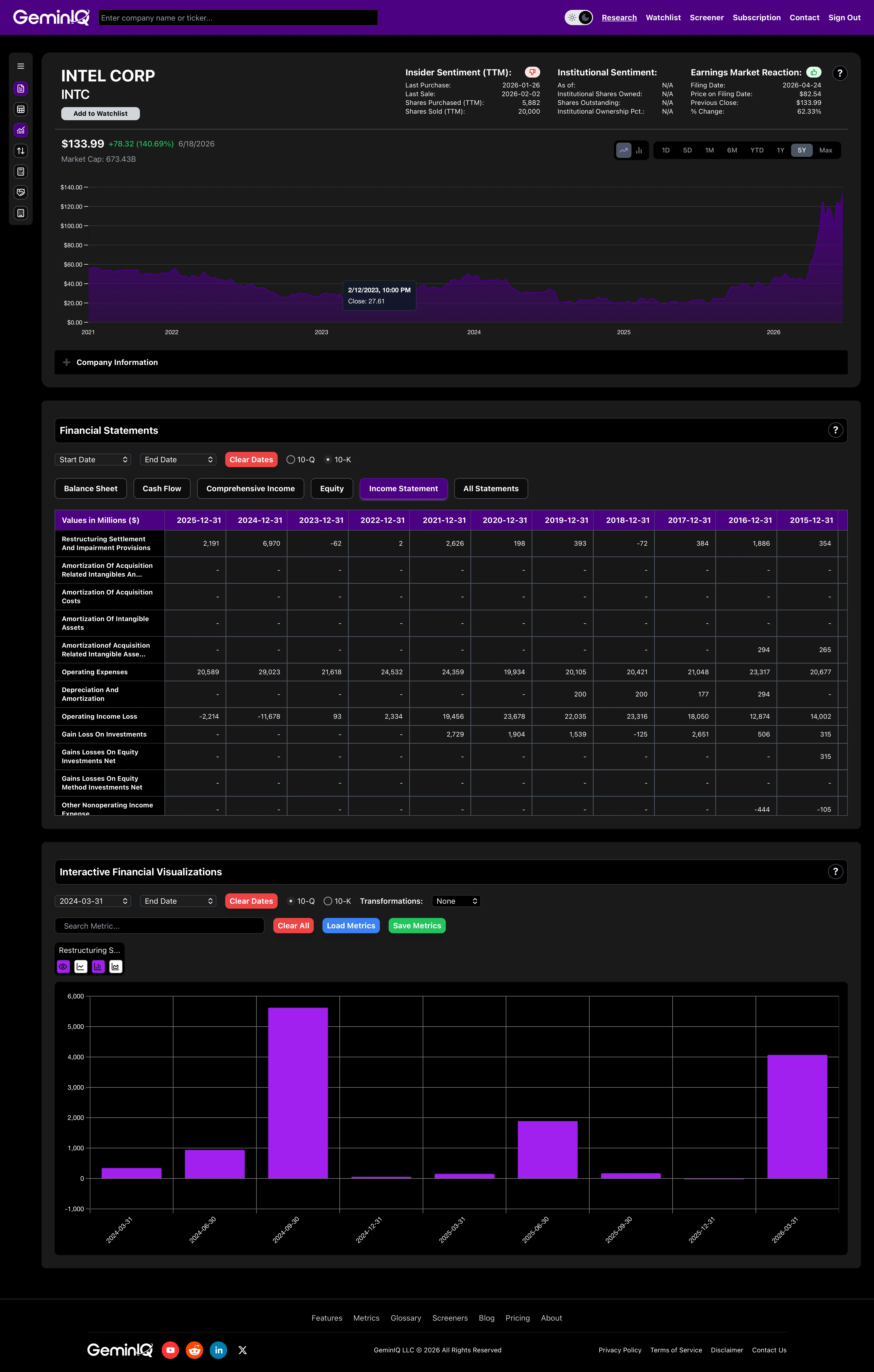

Here is the line item the Computex coverage ignores. Intel has been taking impairment and restructuring charges at a scale that rivals its operating losses.

The Data: GeminIQ pulls the RestructuringSettlementAndImpairmentProvisions line directly from each filing. In FY2024, Intel booked $6.970 Billion in restructuring and other charges — in a single year. FY2025 added $2.191 Billion more. Q1 FY2026 alone added $4.070 Billion. That is $13.231 Billion in write-offs and impairment charges across roughly five quarters, as the company continuously re-values assets from a capacity buildout that preceded the revenue collapse. The $4.07 billion figure in Q1 2026 is precisely what turned gross profit of $5.347 Billion into an operating loss of -$3.136 Billion (OperatingIncomeLoss). Strip the restructuring charge and the business generated roughly $934 million in operating profit. Include it and the net loss was -$3.728 Billion.

The GeminIQ Edge: Standard financial media reported the Q1 2026 earnings miss and moved on. GeminIQ's raw filing data lets you track the cumulative impairment toll quarter-by-quarter — what has been written down, how often, and whether the charges are decelerating or accelerating. The Q1 2026 charge of $4.07 billion represents an acceleration, not a wind-down.

Free Cash Flow: The Number That Doesn't Match the Narrative

The stock surged 31.78% in the month following the Q1 FY2026 filing date. The filing itself showed deeply negative free cash flow.

The Data: GeminIQ's pre-calculated Free Cash Flow for Q1 FY2026: operating cash flow of $1.096 Billion minus capital expenditures of $3.636 Billion equals -$2.540 Billion. On a trailing twelve-month basis through March 31, 2026, operating cash flow was $9.980 Billion against $13.099 Billion in capital expenditures — TTM free cash flow of -$3.119 Billion. This is an improvement from FY2024's -$15.656 Billion TTM FCF, but it remains negative. Intel is still spending more capital than its operations generate. The trailing twelve-month Return on Invested Capital is -3.4%. Every dollar of capital deployed across the business is generating a negative return.

The GeminIQ Edge: Pulling Intel's Free Cash Flow and ROIC side-by-side in GeminIQ's calculated metrics makes the gap between narrative and reality visible at a glance. The capex is declining — $23.944 Billion TTM in FY2024, down to $13.099 Billion TTM through Q1 2026 — but Intel remains FCF-negative, and the stock is up over 30% in the month after the filing that showed it.

The Balance Sheet: Carrying $45 Billion in Debt Through the Transition

Intel's balance sheet reflects the true cost of funding a simultaneous revenue recovery and fab transformation at scale.

The Data: As of March 31, 2026, Intel's long-term debt stood at $43.027 Billion, with $2.004 Billion in short-term debt — a combined $45.031 Billion in total debt. Cash and equivalents were $17.247 Billion, leaving a net debt position of approximately $27.8 Billion. With trailing twelve-month EBITDA of $6.185 Billion, the implied Net Debt-to-EBITDA ratio is approximately 4.5x. For a company still generating negative free cash flow, this is a structural constraint. Total assets were $205.332 Billion, with total equity at $124.989 Billion.

The GeminIQ Edge: GeminIQ computes Net Debt and Net Debt-to-EBITDA directly from the as-filed balance sheet figures, without normalization. The raw number is blunt: Intel is carrying near-peak debt through a period of near-peak uncertainty in its transformation.

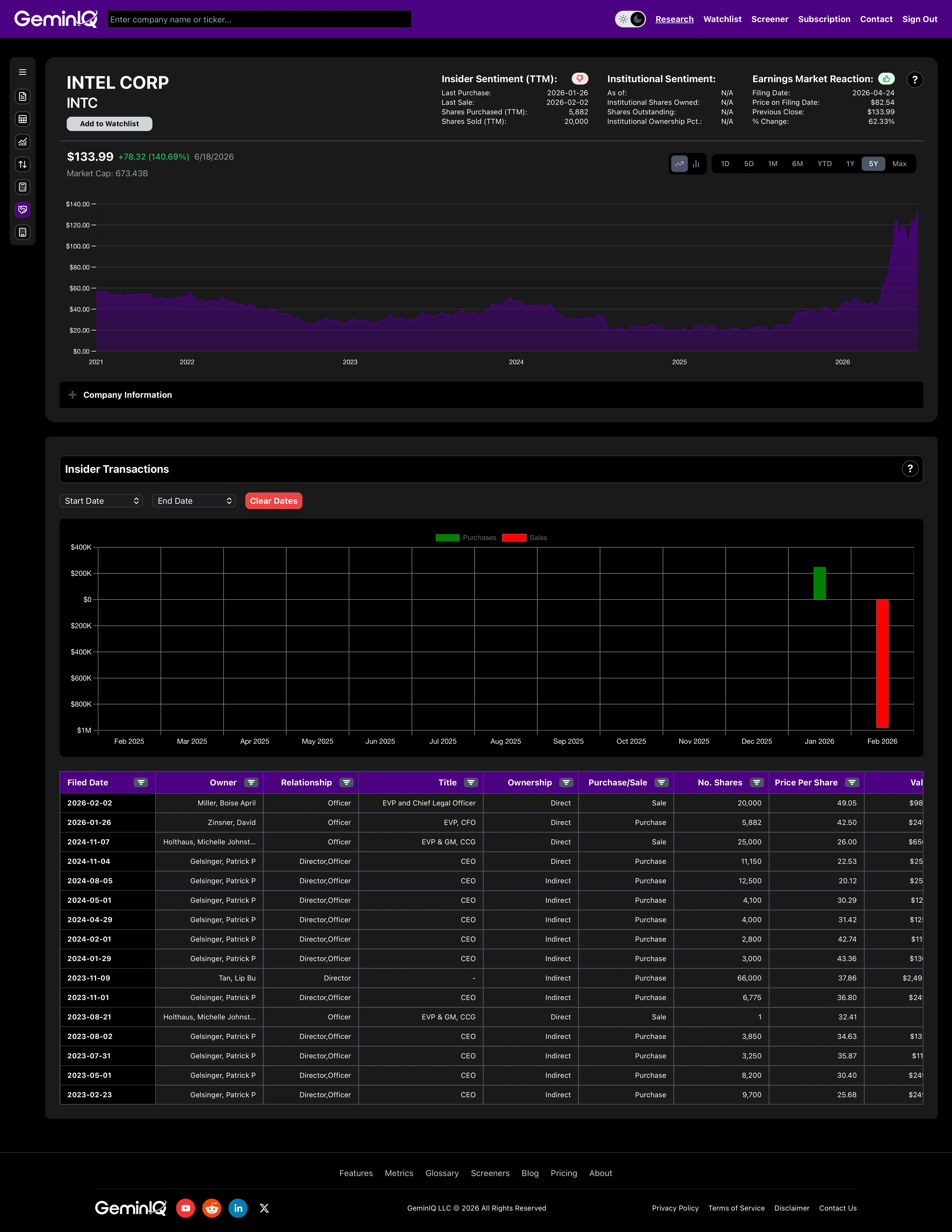

What Are the People Running Intel Doing With Their Own Money?

Insider transactions filed under SEC Form 4 are one of the few signals that financial aggregators routinely obscure through rounding or filing lag. GeminIQ pulls the raw Form 4 data directly.

The Data: In late January 2026, CFO David Zinsner made an open-market purchase of 5,882 shares at $42.50 per share — approximately $249,985 — a directional signal from the person responsible for the balance sheet described above. Seven days later, EVP and Chief Legal Officer Boise April Miller sold 20,000 shares at $49.05 per share, collecting approximately $981,000 in proceeds. The CFO buying and the CLO selling within the same week is a mixed signal that a simple headline screener would miss entirely.

The GeminIQ Edge: GeminIQ's Insider Transactions feed surfaces these Form 4 filings alongside the share price at the time of each transaction. At prices that now look cheap relative to the rally that followed, the divergence between the CFO's conviction buy and the CLO's near-term exit in the same window is exactly the kind of signal that only raw Form 4 data can surface cleanly.

The market has already priced Intel as an AI winner. The Q1 FY2026 10-Q shows a business still losing $3.7 Billion in a single quarter, writing down $4 Billion in assets, and spending more capital than it generates. The turnaround may prove real — but the income statement has not confirmed what the stock price has already assumed.

Research Faster. Invest Smarter.

Most financial websites rely on third-party aggregators that simplify or process data before you ever see it. We built GeminIQ because we believe you deserve a better fundamental analysis tool—one that goes beyond basic price charts and processed numbers. We extract our data directly from SEC 10-K and 10-Q filings to ensure that when you look at a balance sheet or a cash flow statement, you are seeing the numbers exactly how the company reported them. Our goal is to give you the tools to verify the narrative for yourself using clean, traceable data. Start researching now at GeminIQ.com.

All financial figures cited in this article reference Intel Corporation's Q1 FY2026 10-Q (filed April 24, 2026, period ending March 31, 2026). All SEC filings are publicly available at SEC EDGAR.

Disclaimer: The content in this blog is for educational and entertainment purposes only and does not constitute financial, legal, or tax advice. Investing involves risk, including the loss of principal. The views expressed are my own and not intended as financial advice or a guarantee of future performance.