Buffett Stock Criteria: Quality Business at a Fair Price

By Chad Hartman

Published · Last updated

Warren Buffett is the most studied investor alive, and his framework is also one of the most misapplied. The popular version focuses almost entirely on finding cheap stocks — low P/E, low price-to-book, something that looks undervalued by a simple ratio. That is the Benjamin Graham framework, and Buffett spent his early career using it. The shift came in 1972, when Berkshire Hathaway acquired See's Candies for $25 million — roughly 3x book value, far above what the early Buffett would have paid for anything. That price looked wrong by Graham's logic. It turned out to be the most important trade of Buffett's career, not because it was cheap, but because See's was a wonderful business. This post breaks down the five criteria that define Buffett's quality-at-fair-price framework, explains what aggregator data gets wrong on each one, and shows exactly how to run the screen on data sourced directly from SEC filings.

Table of Contents

- The Framework Most Investors Get Backwards

- Criterion One: Return on Invested Capital (ROIC ≥ 15%)

- Criterion Two: Return on Equity (ROE ≥ 15%)

- Criterion Three: A Conservative Balance Sheet (Debt-to-Equity ≤ 0.5)

- Criterion Four: Consistent Earnings Growth (≥ 8% Over Three Years)

- Criterion Five: A Price You Won't Regret (P/E Between 1x and 30x)

- What Financial Aggregators Get Wrong on Each Criterion

- How to Run the Buffett Screen in GeminIQ

The Framework Most Investors Get Backwards

The insight Buffett credits to Charlie Munger is simple to state and difficult to internalize: it is better to own a wonderful business at a fair price than a fair business at a wonderful price. A cigar-butt stock — one cheap enough to squeeze a few more puffs out of before it goes cold — requires you to be right about the exit. A wonderful business, compounding capital at 20% or 25% ROIC for a decade, makes you money whether or not you time anything correctly. The stock price is almost irrelevant if the underlying business keeps earning exceptional returns on every dollar it retains.

The framework that operationalizes this preference has five components: high returns on invested capital, high returns on equity, a conservative balance sheet, consistent earnings growth, and a price that is not catastrophically high relative to current earnings. None of these filters in isolation is sufficient. A business with 40% ROIC and 6x debt-to-equity is not a Buffett-style investment — leverage that high eliminates the margin of safety that quality businesses are supposed to provide. A business with 0.1 Debt-to-Equity and 5% ROIC fails the quality test entirely. All five criteria must be satisfied simultaneously, which is why the screen produces a short list rather than a long one.

The screen has a hard limit, and Buffett himself would name it first. His actual selection process is heavily qualitative: he is looking for durable competitive moats — brands with genuine pricing power, network effects that compound over time, switching costs that make customers reluctant to leave — and management teams with the capital allocation discipline to reinvest earnings at high rates of return for years. A screen can narrow a universe of thousands down to a manageable list of candidates worth investigating. It cannot perform the qualitative analysis that determines whether a candidate belongs in a long-term portfolio. That step requires reading the filing. But standard financial media doesn't read the footnotes.

Criterion One: Return on Invested Capital (ROIC ≥ 15%)

GeminIQ's pre-calculated Return on Invested Capital is the primary quality filter in this framework for a foundational reason: it answers the most important question in investing. For every dollar of capital deployed in this business — by both debt holders and equity investors — how many cents of after-tax operating profit does it generate? A business with a ROIC consistently above its cost of capital is creating economic value. A business earning less than its cost of capital is destroying value, even when it appears profitable on the net income line.

The threshold in this screen is ROIC at or above 15% on a trailing twelve-month basis. This clears the estimated cost of capital for most US companies — typically in the 7% to 12% range — with a meaningful buffer. A ROIC above 25% on a sustained basis is exceptional and almost always signals a genuine, defensible competitive advantage. The kind of business that earns 30% ROIC year after year tends to have structural protection — a brand, a network, a cost structure, a switching cost — that competition has not been able to erode. That is precisely the business Buffett is looking for, and ROIC is the metric that finds it.

Apple illustrates what the high end of this distribution looks like. Apple's trailing twelve-month ROIC registered at 81.7% as of its Q2 FY2026 10-Q (period ended March 28, 2026) — an extreme case reflecting a capital-light, high-margin business running at full compounding power, with an equity base compressed by aggressive buybacks. For most Buffett-style candidates, the threshold is far more modest than that. But the principle is identical: the business must earn more on deployed capital than that capital costs to obtain.

Buffett himself focuses on return on tangible equity, which strips goodwill and acquired intangibles from the invested capital base. For acquisitive companies that have accumulated large goodwill balances, this distinction matters significantly. GeminIQ reports invested capital as-filed, with goodwill visible as a separate balance sheet line, so you can evaluate the return on both total and tangible capital independently. For a complete treatment of the formula, benchmarks, and where the metric breaks, the Return on Invested Capital pillar post covers the full methodology.

Criterion Two: Return on Equity (ROE ≥ 15%)

Return on equity measures profit generated per dollar of shareholder equity. Where ROIC evaluates the return on all capital deployed by both debt and equity investors, GeminIQ's pre-calculated Return on Equity measures specifically what equity holders are earning on the book value of their stake. Buffett has used ROE as a quality signal because, for a business that grows primarily through retained earnings rather than debt issuance, a high ROE means the company is compounding the equity base efficiently. A 20% ROE sustained over a decade means the equity base doubles approximately every 3.6 years — and if earnings multiple stays constant, so does the investor's wealth.

The threshold in this screen is ROE at or above 15%. Paired with a Debt-to-Equity ceiling of 0.5, this filter is designed to isolate businesses where the high ROE reflects genuine operational excellence rather than financial engineering. A company that borrows aggressively to fund buybacks shrinks its equity base, which inflates ROE even if the underlying business is not more profitable. That is why both criteria must be evaluated together. A 25% ROE with a Debt-to-Equity of 3.0 is a leverage play. A 20% ROE with a Debt-to-Equity of 0.2 is a quality business.

One structural limitation is worth flagging directly. Companies with very aggressive share buyback programs sometimes operate with negative book equity, at which point ROE becomes mathematically unreliable — the denominator shrinks toward zero or turns negative, producing extreme or undefined ratios. In those cases, ROIC becomes the primary quality signal, and the screen's earnings growth and P/E filters carry more of the evaluative burden. The screen's design accommodates this by requiring all five criteria to hold, not any single one in isolation.

Criterion Three: A Conservative Balance Sheet (Debt-to-Equity ≤ 0.5)

Buffett has described financial leverage with characteristic clarity over decades of shareholder letters: borrowed money eliminates the margin of safety that rational investing requires. A wonderful business drowning in debt can face forced selling at exactly the wrong moment. A merely adequate business with no debt can survive almost anything. The Buffett framework therefore imposes a strict balance sheet test: total liabilities cannot exceed 50% of total shareholders' equity, expressed as GeminIQ's pre-calculated Debt-to-Equity Ratio at or below 0.5.

This threshold is deliberately conservative by broad market standards. Many respectable companies carry Debt-to-Equity ratios between 1.0 and 2.0 without operational stress. The screen is not trying to find the average public company — it is trying to find the subset whose competitive advantages are so durable that they do not need debt to generate attractive returns. A business with 20% ROIC and zero debt is compounding capital for its owners without transferring any of that return to creditors through interest expense. That structural advantage compounds quietly over time.

The filter also serves as a structural exclusion for capital-intensive sectors where high leverage is a business model feature rather than a risk signal. Banks, utilities, and REITs routinely operate with Debt-to-Equity ratios above 2.0 by design — their business model is, in effect, to borrow at low rates and deploy at higher rates. The 0.5 ceiling appropriately filters them out, since the quality metrics — ROIC and ROE — are not comparably useful for evaluating financial institutions anyway.

Criterion Four: Consistent Earnings Growth (≥ 8% Over Three Years)

A quality business earns high returns on capital. But high returns on a stagnant earnings base are less valuable than high returns on a growing one. Criterion four filters for businesses where net income is genuinely expanding — not in a single exceptional year, but on a sustained three-year basis. The screen requires GeminIQ's pre-calculated Net Income Growth at or above 8% over three years.

The three-year window is intentional. One-year net income can be distorted by a single item: a tax benefit from stock-based compensation, a one-time gain on asset sales, a reversal of a legal reserve. Three years of sustained growth filters out these one-off effects and requires the underlying business to be expanding its earnings power over time. Buffett has consistently stated that he prefers a business earning 15% ROIC with reliable consistency over one that earns 35% in peak years and 5% in troughs. The three-year requirement operationalizes that preference. Consistency is the filter that separates businesses with moats from businesses that had a good run.

The threshold of 8% is not aggressive — it is a floor, not a target. A quality business compounding earnings at 15% or 20% annually over three years clears this criterion easily. The 8% minimum is designed to exclude businesses in structural decline: those whose earnings have grown, in aggregate, less than inflation over three years are not compounding capital for shareholders in any meaningful sense, regardless of what the ROIC number says about a single trailing period.

Criterion Five: A Price You Won't Regret (P/E Between 1x and 30x)

The fifth criterion is the least Buffett-specific of the five, and it requires careful interpretation. A P/E ceiling of 30x is not a Graham "margin of safety" threshold. Graham was looking for stocks at deep discounts — P/E ratios of 8x or 10x, stocks selling below working capital. Buffett's evolved framework tolerates a much higher price for a much better business. Coca-Cola was accumulated in Berkshire's portfolio at more than 15x earnings. Buffett paid a quality premium, not a distress discount. The point of the 30x ceiling is not to find cheap stocks — it is to avoid paying a catastrophically high multiple for even a wonderful business, where the mathematics of compounding cannot catch up with the entry price within a reasonable investment horizon.

The floor at GeminIQ's pre-calculated Price-to-Earnings Ratio of 1x serves a different purpose: it removes companies with negative or near-zero earnings that would otherwise produce mathematically valid but economically meaningless low multiples. A company reporting minimal net income on a multi-billion dollar market cap clears a P/E ceiling of 30x by generating a calculated ratio in the thousands — which is a screener artifact, not a valuation signal. The 1x floor eliminates this class of result entirely.

Two limitations of P/E as a valuation criterion are worth stating plainly. First, P/E is sensitive to one-time items: a large impairment charge or restructuring cost suppresses net income, inflating trailing P/E even if the underlying business is unchanged. Second, P/E does not account for growth. A business growing earnings at 25% annually can justify a 30x P/E far more easily than a business growing at 3%. The P/E criterion in this screen functions as a basic reasonableness check, not a primary quality signal. The first four criteria do that work.

What Financial Aggregators Get Wrong on Each Criterion

Running this screen on aggregated, normalized financial data produces a different set of results than running it on SEC filing data. Each criterion is affected by a specific category of normalization error, and the distortions are not random — they are systematic, introduced by methodological choices that aggregators apply across their entire database.

On ROIC, the most common distortions are the effective tax rate assumption and goodwill treatment. Most aggregators apply a flat 21% federal statutory rate to calculate NOPAT. Companies with significant foreign income, R&D credits, or deferred tax assets routinely report effective rates of 12% to 17%. Applying 21% to those companies overstates tax expense, understates NOPAT, and suppresses ROIC — meaning businesses with genuine international tax efficiency may fail the screen on aggregated data despite passing on as-filed figures. The gap between a 21% assumed rate and a 14% actual rate on a large EBIT base can move the calculated ROIC by 5 percentage points or more for the same company in the same period. GeminIQ uses the actual effective rate derived from the IncomeTaxExpenseBenefit and pretax income XBRL tags filed with the SEC.

On ROE, the primary aggregator issue is the definition of shareholders' equity. Some platforms include minority interests in equity; others exclude them. Some classify preferred equity inside equity; others reclassify it as a liability or mezzanine instrument. These choices change the denominator of the ratio and produce different ROE values for identical underlying businesses. GeminIQ uses Total Shareholders' Equity as reported in the filing — the figure the company itself calculated and submitted to the SEC, with no reclassification.

On stock-based compensation, technology companies in particular carry significant SBC expense that some aggregators add back when calculating adjusted earnings, making ROE and earnings growth appear better than the as-filed numbers. GeminIQ surfaces as-filed net income, and the pre-calculated Stock-Based Compensation to Revenue metric shows exactly what share of revenue is being distributed as equity compensation. For any quality screen that surfaces high-ROIC technology companies, this metric provides essential context: a business reporting 20% net income growth while paying 15% of revenue in stock compensation is sharing a meaningful portion of that growth with employees rather than compounding it for existing shareholders.

On Debt-to-Equity, aggregators make different choices about where to classify hybrid instruments, operating lease obligations, and pension liabilities. Each reclassification moves a balance from one side of the ledger to another, directly changing the ratio. GeminIQ preserves the company's as-filed balance sheet classification, sourced from the XBRL tags Liabilities and StockholdersEquity in the SEC filing.

On net income growth, the aggregator issue is the definition of net income itself. A company that sold a major business division reports the divested segment as a discontinued operation, typically excluded from continuing earnings. Some aggregators strip discontinued operations from both periods to show "cleaner" comparable growth — which, depending on the size of the discontinued segment, produces a materially different three-year growth rate than total as-filed net income. GeminIQ uses total Net Income as reported: not adjusted, not normalized, not stripped of the items a company would prefer analysts to ignore.

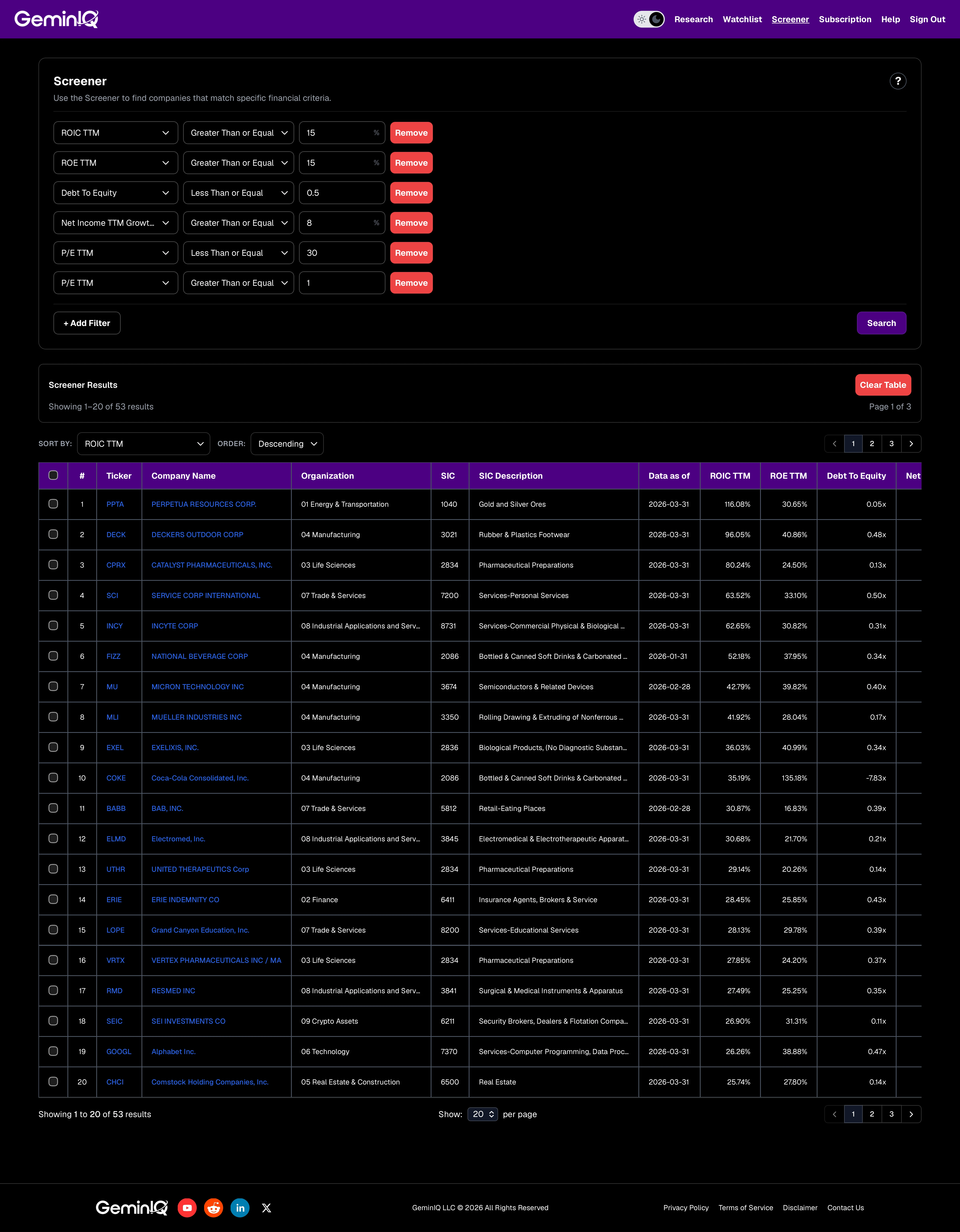

How to Run the Buffett Screen in GeminIQ

The GeminIQ Stock Screener lets you apply all five criteria simultaneously, running on data extracted directly from XBRL-tagged SEC filings. The Buffett-Style screen is available pre-configured at geminiq.com/screens/stock-screeners/buffett-style-screen, or you can build it manually with the following filters:

| Filter | Operator | Value |

|---|---|---|

| ROIC TTM | ≥ | 15 |

| ROE TTM | ≥ | 15 |

| Debt-to-Equity | ≤ | 0.5 |

| Net Income TTM Growth 3Y | ≥ | 8 |

| P/E TTM | ≤ | 30 |

| P/E TTM | ≥ | 1 |

Set Sort By to ROIC TTM, direction Descending, so the highest-quality businesses by return on capital appear first. For each result that clears the quantitative filters, pull the company's Financial Statements in GeminIQ and examine whether ROIC has been stable or improving across at least eight quarters. A company posting a high trailing ROIC that has declined for three consecutive quarters is a materially different situation from one with a consistent or rising trend. The Calculated Metrics trend view surfaces ROIC, ROE, and Debt-to-Equity trended across multiple periods so you can assess whether the numbers that cleared the screen today reflect a durable business pattern or a single strong filing period.

Buffett-style quality is defined by consistency. A business that earns 20% ROIC reliably across a full market cycle is more valuable than one that earns 35% in one year and 8% the next. That is the filter that cannot be faked — and it is the one that requires clean, unprocessed data to run correctly.

Related Reading

- Return on Invested Capital (ROIC): Formula, Benchmarks, and How to Use It — the full methodology behind the primary quality criterion in this screen, including the NOPAT formula, benchmarks, and where the metric breaks.

- Magic Formula Investing Explained — a related quality-and-value screen using ROIC and EV/EBIT combined ranking, and how data normalization distorts which companies appear.

- Piotroski F-Score: The Value Trap Filter — a nine-point financial health checklist that pairs well with any quality screen to eliminate deteriorating businesses that pass on surface metrics.

- Free Cash Flow Yield Explained — why FCF yield complements the P/E criterion for evaluating whether a quality business is trading at a genuinely fair price.

- Value Investing Glossary: Terms, Ratios, and Mental Models Defined — plain-English definitions of every metric and concept referenced in this post.

Research Faster. Invest Smarter.

Most financial websites rely on third-party aggregators that simplify or process data before you ever see it. We built GeminIQ because we believe you deserve a better fundamental analysis tool—one that goes beyond basic price charts and processed numbers. We extract our data directly from SEC 10-K and 10-Q filings to ensure that when you look at a balance sheet or a cash flow statement, you are seeing the numbers exactly how the company reported them. Our goal is to give you the tools to verify the narrative for yourself using clean, traceable data. Start researching now at GeminIQ.com.

All financial figures cited in this article reference Apple Inc.'s Q2 FY2026 10-Q (filed May 1, 2026, period ending March 28, 2026). All SEC filings are publicly available at SEC EDGAR.

Disclaimer: The content in this blog is for educational and entertainment purposes only and does not constitute financial, legal, or tax advice. Investing involves risk, including the loss of principal. The views expressed are my own and not intended as financial advice or a guarantee of future performance.